On March 14th, 2023, I watched EUR/USD spike 180 pips in 40 minutes after the SVB collapse news broke. I was sitting on a $100k prop firm account with a $9,000 daily drawdown limit and a position that was underwater by $7,200 at the worst tick. Heart pounding. One more bad candle and I'd lose the account entirely. That moment crystallized every real difference between prop trading vs retail trading with your own cash. The rules aren't just bureaucratic noise. They reshape every decision you make, every single day.

The $100k prop account with a $9,000 daily limit forces structured discipline—but your own $10k has infinite upside potential. The real question isn't which pays more, it's which fits your risk tolerance.

What You're Actually Comparing Here

Let's be blunt about what these two setups actually are before we run any numbers.

A prop firm account means you pay a fee (typically $300-$600 for a $100k challenge), pass a performance evaluation, and then trade the firm's capital. You keep a percentage of profits, usually 70-90%. You don't risk your own capital beyond that initial fee. But you operate under strict rules: maximum daily loss limits, overall drawdown limits, minimum trading days, sometimes restrictions on news trading or holding over weekends.

A self-funded account is exactly what it sounds like. You deposit your own money at a regulated broker, and you trade it. No evaluation. No rules imposed by anyone. You keep 100% of every dollar you make. You also lose 100% of every dollar you blow.

The tension between these two isn't really about which model is "better" in the abstract. It's about which one fits your specific capital situation and trading style. I've run both simultaneously for over three years, and the answer isn't as obvious as most YouTube channels will tell you.

Prop firms require a small upfront fee ($300-600) for a $100k challenge, but you trade with their capital—not your own life savings.

The Math: $100k Prop vs $10k Personal Account

This is where most comparisons get lazy. Let me give you actual numbers.

Scenario: 5% monthly return on your trading capital

| Factor | Prop Firm ($100k account) | Self-Funded ($10k account) |

|---|---|---|

| Starting capital traded | $100,000 | $10,000 |

| Your upfront cost | ~$540 (challenge fee) | $10,000 |

| Monthly return (5%) | $5,000 gross | $500 gross |

| Your cut | $4,000 (80% split) | $500 (100%) |

| Effective return on YOUR money | 740% annualized | 60% annualized |

| Account termination risk | High (firm rules) | Low (your choice) |

| Scaling speed | Immediate via firm capital | Slow (compound from $10k) |

That $4,000 vs $500 monthly gap is the entire argument for going the prop route when you're undercapitalized. And the math is honestly hard to argue with if you're a consistent trader.

Here's where it gets interesting though. To make $4,000/month on a self-funded account with a 5% return, you'd need $80,000 of your own capital deployed. Most retail traders don't have that sitting around. That's the whole point.

But flip the scenario. If you already have $25,000 in trading capital and you're generating a consistent (but variable) 3-7% monthly return, self-funded trading starts looking very different. At $25k with 5% average, you're making $1,250/month, keeping all of it, with zero risk of account termination from a firm's rulebook. Compound that for 24 months and you're approaching the $80k threshold naturally.

I ran a self-funded account from 2018 to 2020 starting at $8,500. Took me 26 months of consistent trading to get it to $31,000. Slow? Yes. But I never once worried about violating a daily drawdown rule during a choppy week in August 2019 when every trade I touched turned against me.

When you realize $100k of other people's money hits differently than your own $10k.

Risk Profile: Two Very Different Ways to Lose

People talk about risk in prop trading vs retail like there's one type. There are actually two completely different risk profiles here, and confusing them is expensive.

Prop firm risk: termination without warning

With a funded account vs live personal account, your biggest danger isn't losing money. It's losing access. Prop firms can and do terminate accounts for rule violations, even profitable ones. Hit your daily loss limit on a Thursday while you're up $8,000 on the month? Account closed. Miss a minimum trading day requirement? Account closed. Some firms have added clauses about "consistency rules" where if one single day's profit exceeds 30-40% of your total profit, they flag it or void the payout.

I got hit by this in 2022. I had a $50k account with a well-known prop firm (won't name them, but they're still operating). Made $3,200 in one day during a CPI release trade, which was about 45% of my monthly profit. Payout was delayed and partially disputed. Took six weeks to resolve. Read the fine print. Every word of it.

Self-funded risk: slow bleed or sudden blow-up

With self-funded trading, the risk is simpler and in some ways more honest. You can blow the account. Full stop. No firm's rules protecting you from yourself. I've seen traders with excellent prop firm track records absolutely crater their own accounts because the psychological guardrails were gone.

There's also the slower, less dramatic risk: the grinding drawdown. You start with $15,000, you're down 20% after a bad six weeks, now you're trading $12,000 and your position sizing is mentally compromised. No one terminates your account. You just slowly erode your own edge.

The honest answer is that neither risk is "worse." They're just different. Prop firm risk is sudden and external. Personal account risk is slow and internal.

The moment you understand that blowing up a prop account and blowing up your life savings aren't the same thing.

The Psychology Nobody Talks About

Rules pressure vs freedom stress. Both will mess with your head. Just in opposite ways.

Trading a funded account vs live personal account changes your psychology at a fundamental level. When you're in a prop firm account, every losing day carries a secondary question: "Am I close to my daily limit?" That question doesn't exist in pure self-funded trading. It creates a specific type of distorted decision-making where you avoid perfectly valid setups because you're mentally calculating drawdown headroom instead of actual probability.

I've deliberately cut trades short on prop accounts not because my analysis said to, but because I was already $1,800 into a $2,500 daily limit and didn't want to risk the account on what was actually a strong setup. That's not trading. That's rule management disguised as trading.

On the flip side, freedom stress is real. When you're self-funded trading with no rules, no accountability structure, and no one watching, the psychological discipline has to come entirely from inside. A lot of traders discover they didn't actually have that discipline. They thought they did. The prop firm rules were doing half the work.

The traders who thrive in self-funded accounts tend to have either: extensive experience (7+ years minimum in my observation), or very small position sizes relative to account equity so drawdown never feels catastrophic. The ones who thrive in prop firms tend to be systematic traders where the rules actually align with their strategy's natural parameters.

Tax Reality for US Traders

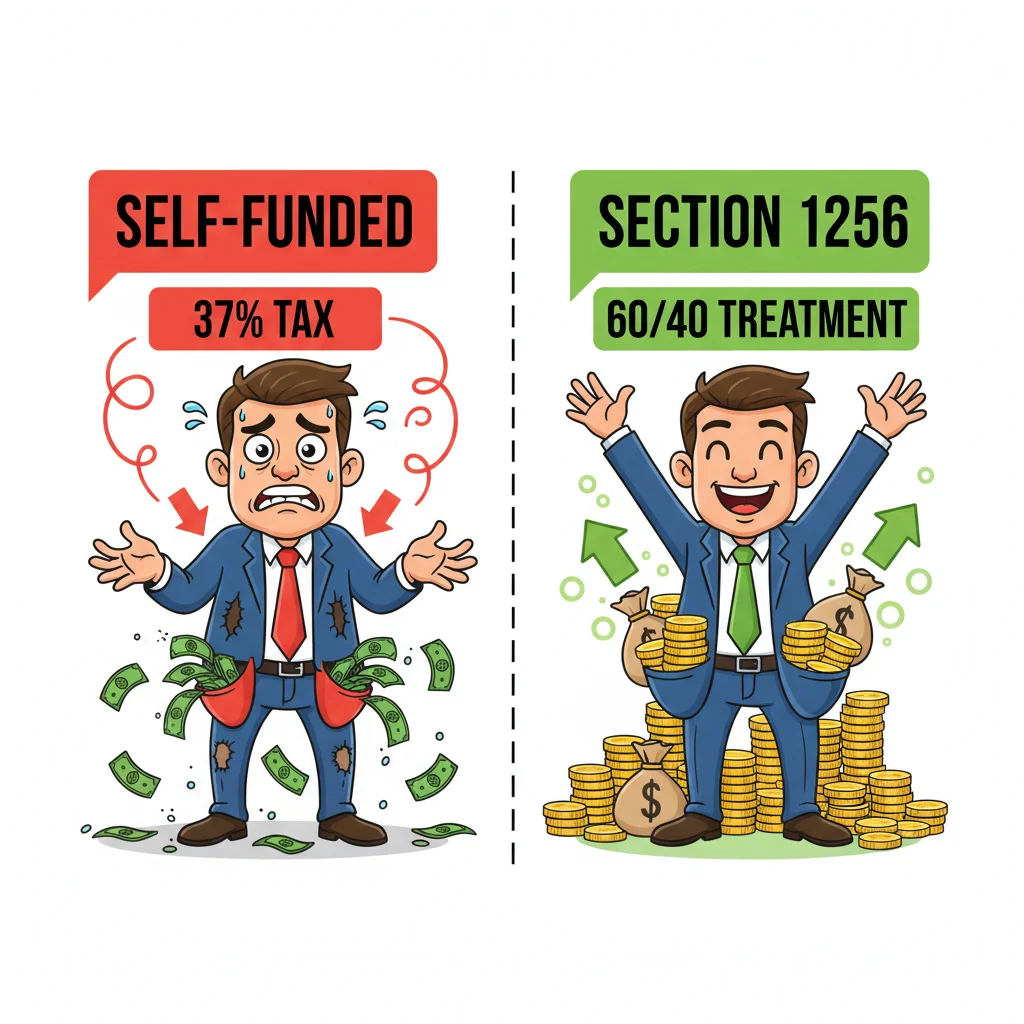

This section matters more than most people think, and the difference between prop firm vs personal account treatment can add up to thousands of dollars a year.

Self-funded account taxation: In the US, forex spot trading profits are taxed under Section 988 by default (ordinary income rates, up to 37%). You can elect Section 1256 treatment for 60/40 capital gains treatment, but you must make that election before the tax year starts. Under 1256, 60% of gains get long-term capital gains rates (0%, 15%, or 20% depending on your bracket) and 40% get short-term rates. For most active traders in higher brackets, this election saves real money.

Prop firm taxation: Here's where it gets messier. With most prop firms, you're classified as an independent contractor. Your payouts are reported on a 1099-NEC. That means you're paying self-employment tax (15.3% on top of income tax) on top of your normal rate. A $48,000 annual prop firm payout could easily hit an effective tax rate of 38-42% for someone in the 22% bracket once you factor in self-employment tax.

The silver lining: as a 1099 contractor, you can deduct legitimate business expenses. Your platform fees, data subscriptions, home office (if used exclusively for trading), your challenge fees, they can all potentially be deductible. Talk to a CPA who specifically handles traders. Not a general accountant. A trader-specific CPA.

One thing that catches prop firm traders off guard: some offshore firms don't issue 1099s at all. That doesn't mean the income is non-taxable. It means it's your responsibility to report it. The IRS doesn't care that your prop firm is based in the Cayman Islands.

US forex traders can save thousands annually by electing Section 1256 treatment for 60/40 capital gains rates instead of defaulting to ordinary income taxation up to 37%.

When Prop Trading Is the Right Call

Go the prop firm route if you fit this profile specifically.

You have under $5,000 in trading capital and you're consistently generating 8% or more monthly returns in demo or small live accounts. That combination means you have the skill but not the capital, which is exactly the gap prop firms fill. At 8% monthly on a $100k account with an 80% split, you're making $6,400/month from a $540 investment. No amount of self-funded compounding gets you there faster from a $5k starting point.

Also consider prop trading if:

- Your strategy is highly systematic with defined stop losses that naturally stay within typical drawdown limits (2% daily stops fit neatly inside a 5% daily drawdown rule)

- You have a track record of at least 6 months of consistent results, not just a hot streak

- You're comfortable with the counter-party risk of the firm itself (research their payout history before committing any challenge fee)

- You want the structure and accountability that external rules provide

One thing I'd add from experience: the best prop firm traders I've seen treat the funded account as one piece of their operation, not their entire identity. They keep a small personal account running alongside it. Keeps the skills sharp without the firm's rulebook overhead.

When prop trading finally pays off and you're building toward that funded account dream.

When Your Own Capital Wins

Self-funded trading is the right call in more situations than the prop firm marketing machine wants you to believe.

If you have over $20,000 in dedicated trading capital, the math starts shifting meaningfully. At $20k with a 5% monthly return, you're making $1,000/month keeping 100%, vs the prop firm alternative where you'd make $4,000 but give 20% away and risk termination. Yes, the prop firm number is bigger, but consider: you're compounding $20k at 5% monthly and in 14 months you have roughly $40k. In 28 months you're approaching $80k. You now earn more per month than a $100k prop account with an 80% split, with no termination risk and no rulebook.

Also go self-funded if:

- Your returns are variable (some months 1%, some months 12%). Prop firms' consistency rules punish this profile hard.

- Your strategy involves holding trades over weekends, trading major news events, or using unconventional instruments some firms restrict

- You want to build genuine, transferable trading capital that compounds over years

- You trade options or other instruments that most prop firms don't support

The compounding math in self-funded trading is genuinely powerful if you have the patience. I know a trader in Dallas who started with $22,000 in 2019, never touched a prop firm, and was at $118,000 by early 2024. Boring story. No YouTube thumbnail material. But real money that's actually his.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Forex and CFD trading carries significant risk of loss. Past performance is not indicative of future results. Always do your own research and consider your financial situation before trading. Never risk money you cannot afford to lose.